Financial Markets Posts on Crowch

Economic instability has become one of the most pressing and emotionally charged issues of the past year. Across the globe, millions of people are grappling with the consequences of inflation, rising prices, currency devaluation, economic slowdowns, and the ripple effects of international crises. While fluctuations in the economy are a natural part of any economic system, the current situation is being felt with unusual intensity due to the simultaneous impact of multiple destabilizing factors — both domestic and global.

The rising cost of living is one of the most immediate and tangible effects. Food, housing, transportation, healthcare, and utilities have all become significantly more expensive in many regions. For middle-class families, this means cutting back on non-essential spending and adjusting budgets to cover basic needs. For low-income households, it can mean choosing between heating and groceries, between education and medical care. Inflation rates in some countries have reached levels not seen in decades, eroding purchasing power and threatening the financial stability of entire communities. Even those who once felt relatively secure are now reconsidering their savings, investments, and long-term plans.

Alongside inflation, the labor market has undergone a major transformation. The aftershocks of the COVID-19 pandemic, combined with the acceleration of digitalization and automation, have reshaped the way people work. Remote work has become widespread, but so has job precarity. Freelance work, temporary contracts, and gig-based employment have grown — offering flexibility for some, but creating insecurity for many others. Workers fear job loss, reduced hours, or stagnant wages, while employers seek to balance cost-saving with productivity. Many professionals, especially in traditional industries, are being forced to retrain or pivot to entirely new fields. Younger generations are entering the workforce under especially difficult conditions: high competition, low entry-level salaries, and limited long-term prospects contribute to growing anxiety and burnout.

Compounding these domestic issues are significant global influences. Ongoing geopolitical tensions, trade disruptions, and military conflicts have deeply affected energy prices and supply chains. The cost of oil, gas, and raw materials continues to fluctuate unpredictably, leading to higher manufacturing costs and delays in production. In many countries, reliance on imports has made local economies particularly vulnerable. Moreover, the lingering consequences of the COVID-19 pandemic are still being felt in key sectors such as tourism, hospitality, small business, and logistics, slowing recovery efforts and increasing debt burdens.

These economic stressors do not exist in a vacuum — they deeply affect the psychological well-being of individuals and the social fabric of communities. Chronic financial stress has led to rising levels of anxiety, depression, and social tension. People are losing trust in institutions that seem unable or unwilling to provide effective support. The gap between rich and poor continues to widen, fueling political polarization and a sense of injustice. In some regions, protests and labor strikes have become more frequent as citizens demand fairer policies and greater transparency from their governments.

In the face of this uncertainty, societies must focus not only on economic measures but also on building resilience and solidarity. Improving financial literacy, supporting innovation and entrepreneurship, investing in education and retraining, and creating safety nets for the most vulnerable are all essential steps. Governments must act with clarity and compassion, while citizens need to stay informed, adaptable, and engaged. Economic instability is not just a test of policy — it is a test of collective strength, empathy, and long-term vision. The way we respond today will shape the kind of world we live in tomorrow.

Let’s be honest: if you had told me in 2015 that by 2025 the United States would be fighting to defend the relevance of the U.S. dollar on the world stage — I probably would’ve smirked, sipped my overpriced coffee, and gone back to reading the Fed minutes.

But here we are.

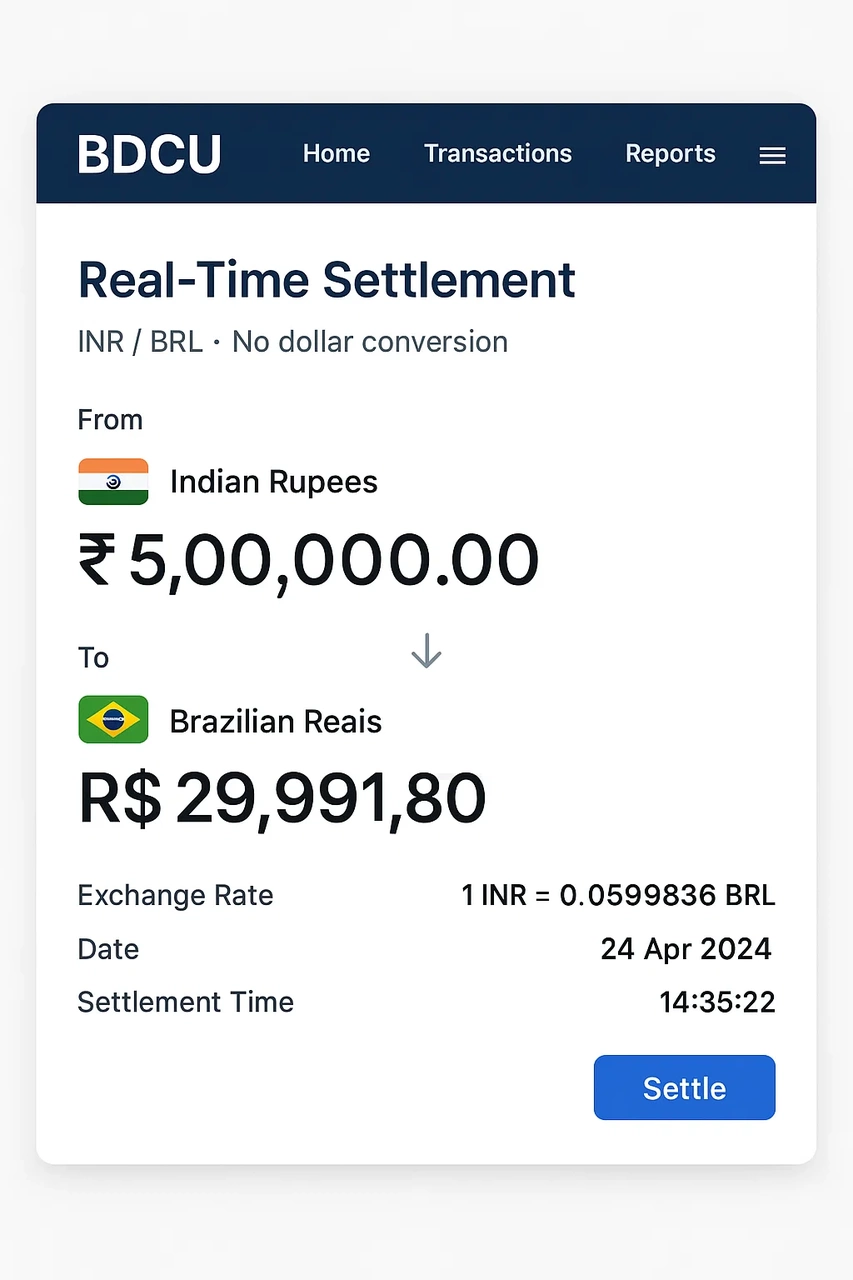

This summer, the BRICS+ coalition — now expanded to include Saudi Arabia, Indonesia, Nigeria, and Turkey — officially launched the BRICS Digital Clearing Unit (BDCU), a blockchain-based trade settlement system designed to bypass the SWIFT network, minimize dollar dependency, and solidify a multipolar financial world.

This is more than a tech upgrade. It’s a financial revolution, one that reorders how power, trust, and risk are distributed in the global economy. And it may well be the most significant shift in monetary geopolitics since Nixon closed the gold window.

The Beginning of the End (of Dollar Hegemony)?

The U.S. dollar has been the world’s reserve currency for nearly 80 years. That dominance gave America the ability to finance deficits cheaply, enforce sanctions effectively, and steer global monetary policy from behind closed doors in Washington.

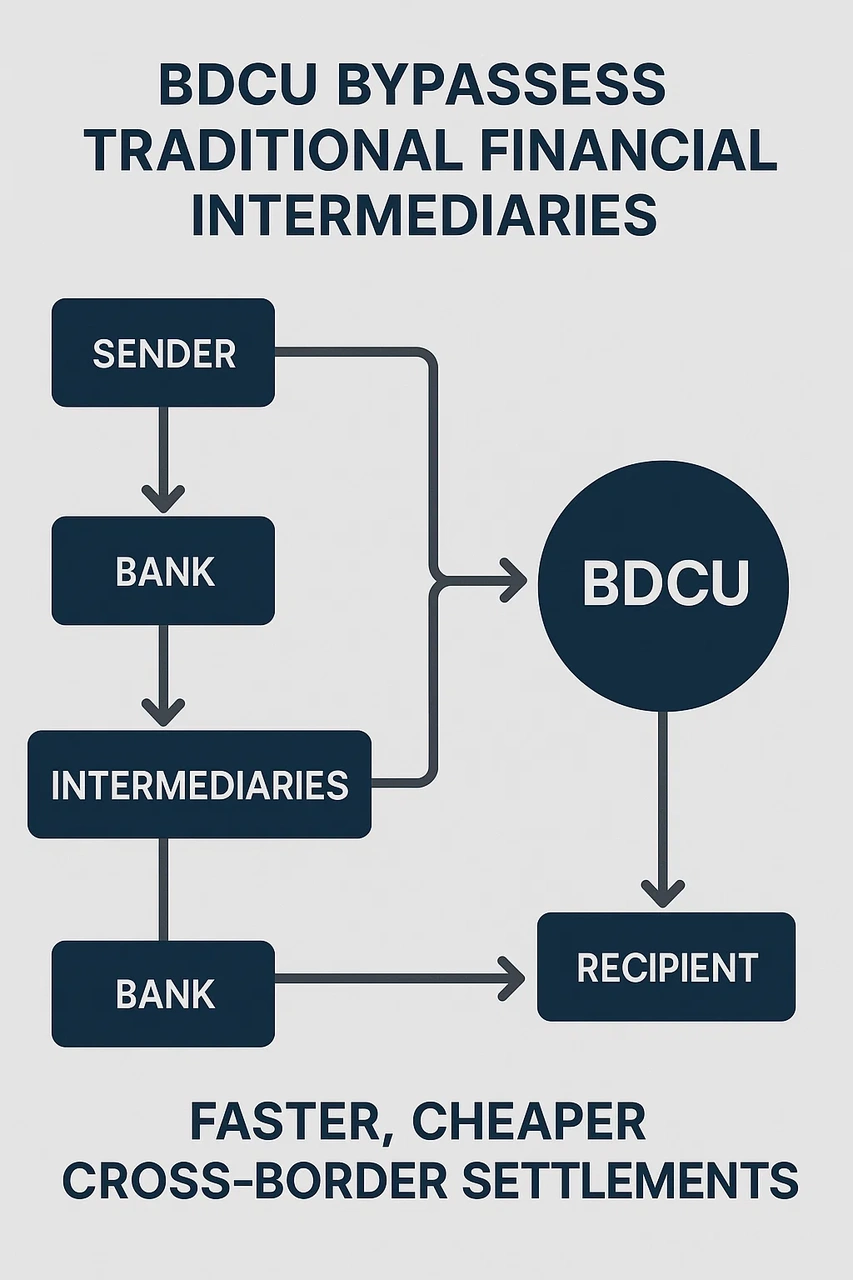

But cracks have been forming. Russia’s ejection from SWIFT. China’s digital yuan pilot. African nations demanding fairer loan terms outside IMF frameworks. Even France, earlier this year, settled a gas shipment from Qatar in renminbi. So when BRICS+ leaders unveiled the BDCU this June, it wasn’t just symbolic — it was practical. A way for nations to conduct smart contract–based trade, with currencies of their choice, governed by a shared digital protocol. No middlemen. No dollar. No Western veto.

And just like that, the foundations of dollar supremacy feel shakier than ever.

A Shift in Trust: From Institutions to Protocols

For years, the global economy relied on institutions like the World Bank, IMF, and BIS to facilitate cooperation and impose order. But in 2025, trust is being redefined — not around institutions, but infrastructure.

The BDCU isn’t just faster or cheaper. It’s programmable. That means trade rules, tax compliance, sanctions, and even environmental standards can be coded directly into transactions. For example, a shipment of palm oil from Indonesia to South Africa could automatically verify deforestation status and carbon intensity before payment clears.

It’s efficient. Transparent. And dangerously seductive. Because while Western policymakers debate regulation, the BRICS+ economies are out here writing the new rules of financial trust — one line of code at a time.

Can the West Catch Up — Or Should It Adapt?

The U.S. response so far has been a mix of concern and confusion. The FedNow+ real-time payment network launched this year, but it’s still domestic. The digital dollar pilot is bogged down in political fighting over privacy and surveillance.

Europe, meanwhile, is watching its banking sector erode as emerging nations build direct trade links without touching the euro or dollar.

And here’s where things get tricky. The West can’t simply ban these systems — they’re open-source, decentralized, and increasingly too large to ignore. Nor can it outcompete them using legacy frameworks from the 20th century. Instead, Western economies might need to redefine their value proposition. That means doubling down on legal protections, contract enforcement, intellectual property, and innovation — things that can’t be easily tokenized or copied. Because in a world where financial plumbing is open to all, power comes not from controlling the pipes — but from offering the most trusted water.

What This Means for the Rest of Us

I’m not a central banker. I’m a guy who loves markets, macro, and the stories behind every spreadsheet. And here’s what I think: This shift isn’t just about geopolitics. It’s about access. The BRICS+ model empowers small and medium-sized nations — and even businesses — to transact without fear of financial exclusion. It lowers costs. Reduces friction. And forces legacy powers to compete for relevance, not assume it.

It also raises tough questions: Who gets to write the code that governs trade? What happens when economic sanctions can be bypassed with a few keystrokes? Will this lead to fragmentation, or eventually to pluralistic integration?

We don’t have answers yet. But here’s the truth no one in D.C. wants to hear: the dollar is no longer inevitable.

It’s optional.

Back in January, when the Global Economic Forum in Singapore released its declaration on autonomous financial oversight, most of us finance nerds leaned in. The idea? That in an era of AI-powered trading, risk modeling, and decentralized finance, the biggest threat isn’t irrational investors — it’s outdated human regulation.

Fast forward to June 2025, and we’ve entered a new era: AI-managed financial governance. From monetary policy tweaks to fraud detection and even ESG enforcement, intelligent systems are now officially embedded in economic steering. And while it feels exciting — even efficient — the philosophical questions it raises are impossible to ignore.

The Birth of “Smart Regulation” — and the Quiet Death of Lag

Let’s rewind. In 2024, three major financial crises happened because regulatory action couldn’t keep up with algorithmic activity: the flash crash in Southeast Asian markets caused by mispriced carbon futures, the synthetic commodity bubble in sub-Saharan Africa, and the decentralized insurance liquidity collapse in LATAM.

In each case, AI-driven systems outpaced human oversight.

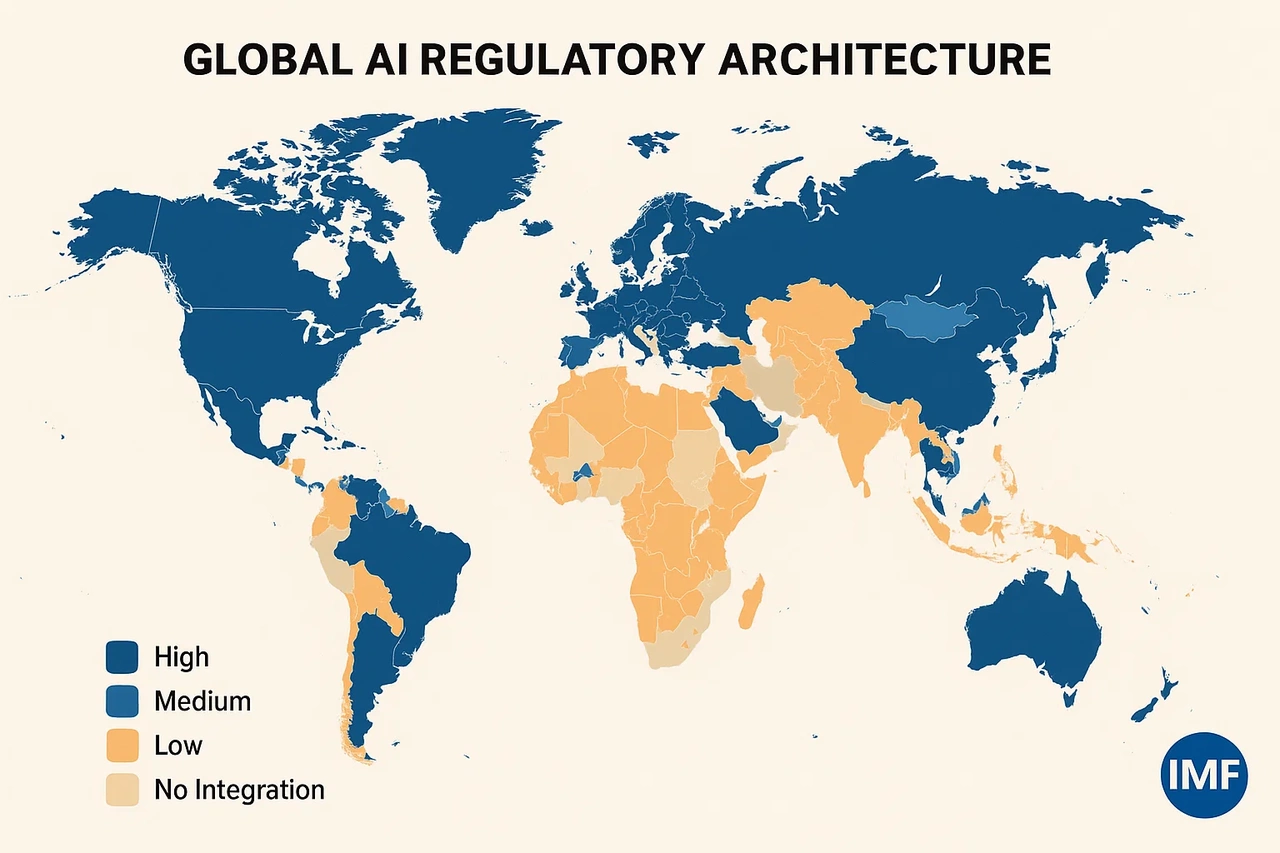

In response, countries like Germany, Singapore, and Brazil started running parallel regulatory pilots powered by machine learning. By 2025, the IMF endorsed the use of Autonomous Supervisory Systems (ASS) — yes, someone really should’ve thought that acronym through — to analyze risk exposure and suggest automatic intervention protocols for central banks.

The promise? Fewer crashes. Faster corrections. Data-driven ethics. The risk? Decisions without debate. Corrections without accountability.

Finance by the Numbers — or by the Values?

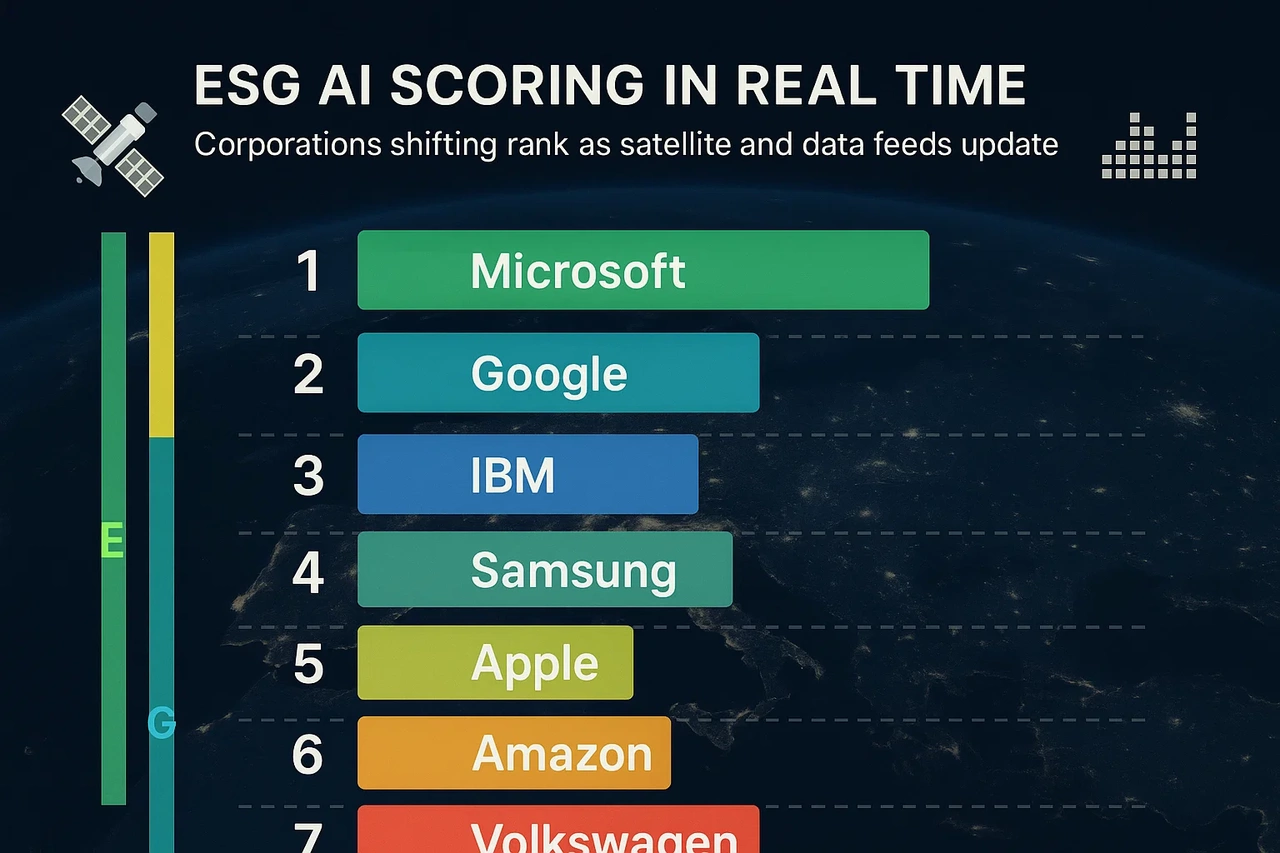

Here’s where I get both excited and uneasy. One of the most radical shifts this year was the AI-enforced ESG scoring mandate adopted in the EU and Canada. Using satellite imagery, corporate disclosures, and real-time social sentiment scraping, companies are now given dynamic ESG scores that directly affect access to loans and tax breaks.

In theory, it’s brilliant. No more greenwashing. No more lobbyist-influenced blind spots.

But I couldn’t help but think: Whose ethics are coded into this system? What happens when an algorithm penalizes a small manufacturer in Eastern Europe for labor practices based on standards it learned from Fortune 500 datasets?

We’ve created a system that’s efficient, but not always empathetic. And while it’s tempting to say "trust the data," we need to ask who’s labeling the training sets, who’s weighting the priorities, and who ultimately benefits. Because in 2025, finance is no longer just about money — it’s about algorithms enforcing morality.

The Digital Bretton Woods?

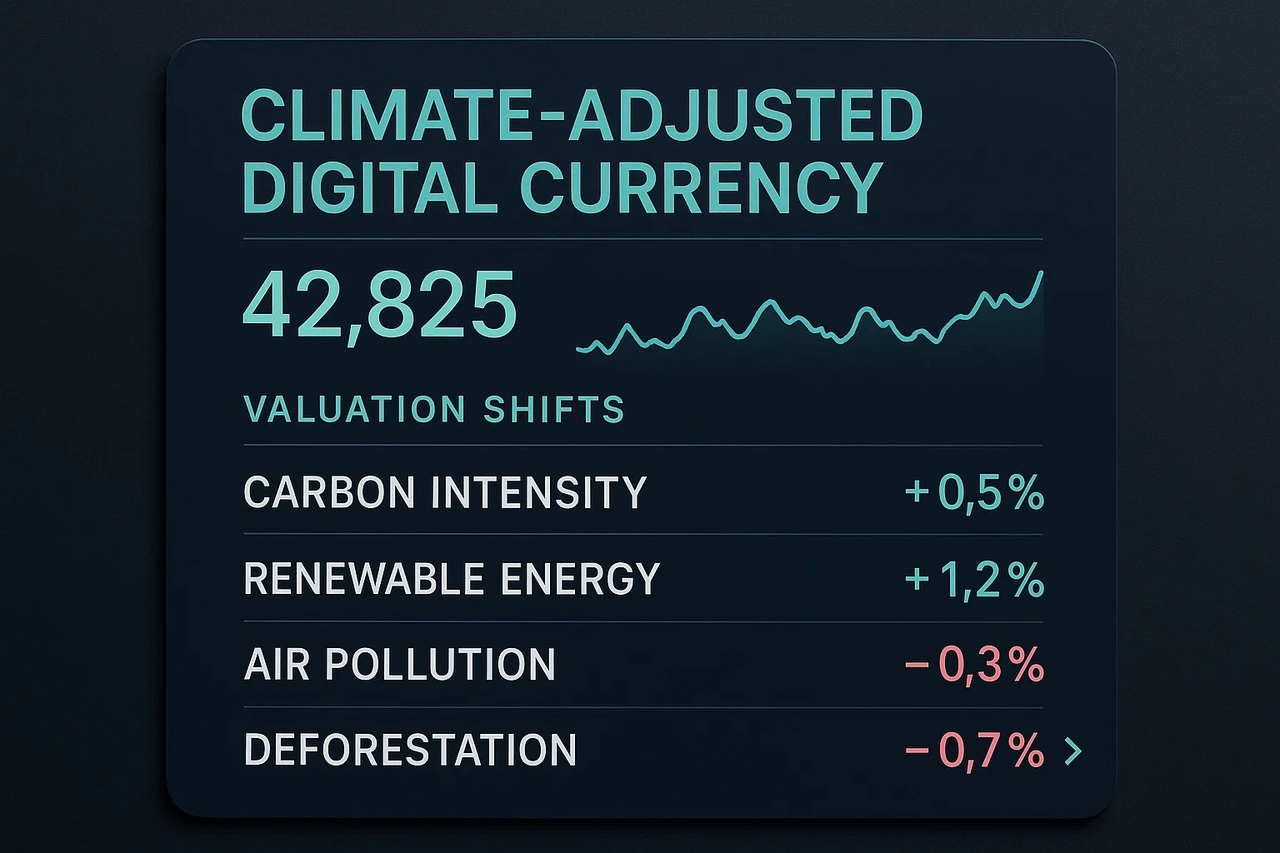

In April, I attended a virtual roundtable titled “Decoding the New Standard”, where finance ministers, AI ethicists, and token economists discussed whether we’re moving toward a digital Bretton Woods — a new global economic order shaped not by gold or GDP, but by code, consensus, and compute power. And here’s what’s wild: for the first time, digital currency frameworks are being tied to climate performance.

Imagine this — a country’s central digital currency (like the e-euro or DUSDR) can devalue if national emissions targets are exceeded, or strengthen if carbon drawdown thresholds are met.

It’s bold. It’s technocratic. And it might be the only way to force accountability into financial systems that have ignored planetary cost for decades.

But it also introduces new instability. What happens when a wildfire — a random natural disaster — tanks your national currency? Are we creating a fairer market, or just a more volatile one?

Where Does This Leave Us?

As a young guy who loves spreadsheets, market cycles, and economic theory — I’m genuinely fascinated by what’s unfolding in 2025. We’ve spent decades saying the market is rational, self-correcting, and largely ungovernable. Now we’re watching the rise of tools that actually make it governable — but in ways that often remove the human from the loop.

We’re replacing regulators with neural nets, central banks with logic chains, and policy with predictions. It’s efficient. It’s elegant. But it’s also deeply unsettling. Because economies aren’t just data. They’re people, cultures, fears, aspirations, and irrational choices. So the real question for the second half of 2025 isn’t how smart the system gets — it’s how human we allow it to remain.